2025 Technology & Market Prediction Evaluation

Taylor Grenawalt

Director, Research & Insights

December 18, 2025

5 min

At the outset of the year, the Vation Ventures Research & Insights (R&I) team established a set of forward-looking 2025 Technology & Market Predictions designed to frame one of the most consequential years yet for AI, infrastructure, security, and capital markets. Reflecting a diverse but deeply interconnected set of themes, our forecasts and predictions were based on the expectation that over the course of the year, these domains would collide and play off one another in ways that would reshape the physical and digital foundations of technology and the enterprise landscape.

Across our ten 2025 predictions, the R&I team achieved an average score of approximately 2.6 out of 3, equating to 87% prediction accuracy and an improvement from an accuracy score of 80% in 2024. Our highest-conviction theses, spanning cybersecurity, infrastructure, and emerging technology advancement, were strongly validated by record IPO and M&A activity, multi-gigawatt infrastructure commitments, unprecedented energy and fusion funding, escalating cyber incidents, and step-change improvements in multimodal and quantum benchmarks.

At the same time, several predictions proved directionally accurate but more muted than anticipated: private market liquidity improved without fully resolving the exit drought, regulatory pullback manifested as modest recalibration rather than wholesale deregulation, labor disruption skewed toward sector-specific volatility rather than broad systemic unrest, and the defense/telecom/space boom materialized unevenly, with defense and space outpacing telecom.

Yet the year and our prediction scores also underscored the persistent and inherent unpredictability of policy environments, macroeconomic constraints, and labor-market responses, each tempering or refracting certain expected developments. Nonetheless, the overarching narrative of 2025 is one of convergence, with compute, energy, security, and intelligence coalescing into a new architectural era that will define competitive advantage for years to come.

.png)

Accelerating Cybersecurity Market Momentum

Score: 3

The cybersecurity sector decisively outperformed expectations as IPO activity, M&A consolidation, and sustained venture investment converged to produce one of the strongest market acceleration cycles on record.

The cybersecurity market’s continued acceleration in 2025 was underscored by a surge in public-market readiness and performance, highlighted by 26 public listings in 1Q25 and Netskope’s high-profile $992 million IPO debut in 3Q25. Complementing this momentum was a sharp increase in platform-driven M&A activity, with landmark transactions such as Google’s acquisition of Wiz and Palo Alto Networks’ multibillion-dollar deals, including CyberArk and Protect AI, contributing to the total 2025 cybersecurity M&A value rising to $63.8 billion and representing more than double the prior year’s $26.2 billion. Global venture funding also reflected a sustained conviction in the sector, with 2025 investment levels reaching $12.8 billion, surpassing even the strong deployment experienced the previous year. Collectively, these developments coincide with rising enterprise demand driven by expanding risk surfaces, AI-enabled threat velocity, and intensifying compliance and resilience requirements. Taken together, the sector’s healthy IPO pipeline, record-breaking consolidation, and continued private capital inflows reinforce the continued market acceleration resulting from evolving risk surfaces, market pressures, and enterprise dynamics.

Private Market Liquidity Release

Score: 2

While exit activity and IPO volumes improved materially in 2025, liquidity conditions fell short of a full recovery, delivering only a partial release of the anticipated private-market bottleneck.

Although 2025 exhibited rebounding improvement in exit activity and IPO markets, which improved liquidity dynamics, the distribution drought failed to be quenched to the extent anticipated. According to PitchBook, as of 3Q35, 35 VC-backed US IPOs of 2025 have generated $87.4 billion in proceeds, already more than double the prior year and surpassing the past three years combined. Furthermore, VC distribution yield has continued to improve throughout the year, rising from a near-historic low of 6.5% in 4Q24 to an estimated 12.7% in 3Q25. Alongside VC dynamics, global private equity IPO and exit activity have also improved, with the latter reaching more than $460 billion and representing a nearly 30% increase compared to last year. Nonetheless, despite the improving dynamics and liquidity landscape, the larger and broader rising tides we expected failed to materialize.

.png)

Competition-Focused Regulatory Pullback

Score: 2

Regulatory easing progressed more modestly than expected, with selective recalibration rather than broad rollback shaping the 2025 policy environment for AI and emerging technologies.

Despite early 2025 and 2024 posturing, the expected rollback of increasingly aggressive technological regulatory scrutiny was more modest and contained than initially projected. In Europe, the EU Commission recently unveiled a Digital Omnibus package, which is designed to streamline compliance and reduce bureaucracy in the GDPR, AI Act and ePrivacy rules. In the US, despite several attempts by the Trump administration and congressional Republicans to adopt a hands-off regulatory approach to AI, including a proposed moratorium on state-level AI laws and regulations, these provisions and proposals have consistently failed to gain the necessary support. However, the Trump Administration has countered existing regulatory frameworks, including rescinding the Safe, Secure, and Trustworthy Development and Use of AI Executive Order signed by President Biden. From this, alongside the absence of any significant new regulatory framework implementations, we can see a continued global trend toward loosening regulatory restrictions around AI and emerging technologies as governments attempt to balance innovation leadership with security and safety.

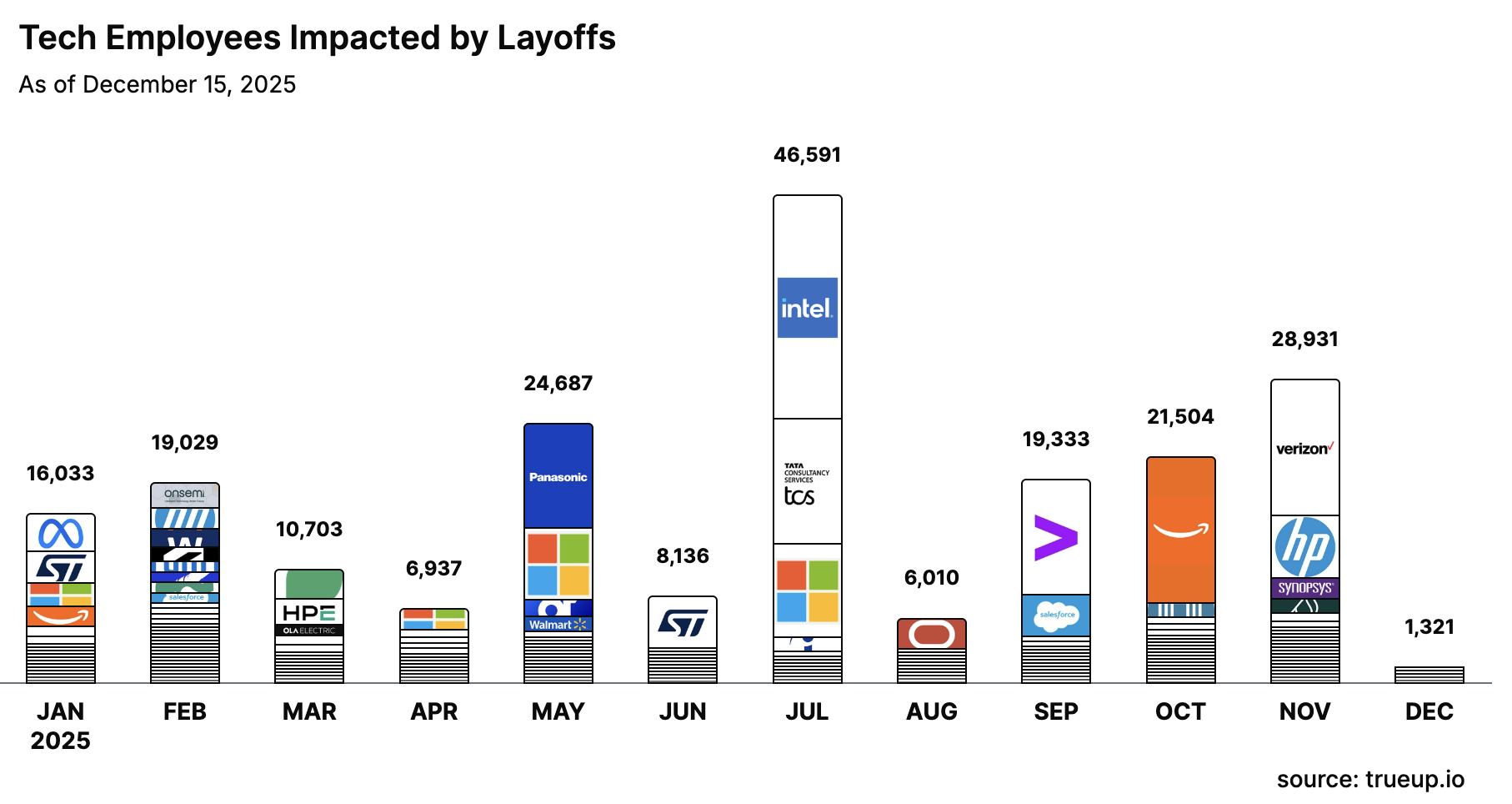

Labor Strain & Volatility

Score: 2

AI-driven displacement and sector-concentrated layoffs intensified workforce strain, though the overall severity remained tempered by reduced strike activity and uneven cross-industry impact.

As expected, AI continued to produce disruption across the workforce and labor markets, with largely sector-concentrated impacts and activity tempering prediction outcome accuracy. Through the first seven months of 2025, there were more than 10,000 US job losses explicitly linked to AI displacement and contributed to a broader 806,000 private-sector layoffs, the most significant amount for that time period since the COVID-19 pandemic. As part of this, more than 89,000 jobs were cut in tech, representing a 35% rise in displacement compared to last year and indicative of sector-driven labor volatility. Based on the initial November and projected December layoff numbers, 2025 is expected to exhibit the highest annual layoff rate since the pandemic, with approximately 1.2 million layoffs forecasted for the 11 months ending in November, representing a more than 50% increase from the same period last year. Alongside the technology industry, the manufacturing industry also experienced further strain throughout the year, with mounting employment declines, structural imbalances, and growth imbalances resulting from persistent skill gaps and labor shortages driven by reshoring. However, the more than 40% decline in labor strikes and related actions, alongside largely industry-concentrated disruption and strain acceleration, served to contain the severity and fulfillment of anticipated strain and volatility.

Data Center Expansion

Score: 3

Hyperscalers and AI-first companies ignited an unprecedented wave of mega-scale data-center buildouts, establishing 2025 as a structural turning point in compute infrastructure expansion.

2025 saw a dramatic acceleration in data-center expansion, led by hyperscalers and AI-first firms doubling down on frontier-model infrastructure, underscoring the massive scale of compute demand and operational transformation. According to Crunchbase data at the end of 3Q25, US VC investment activity in data center technology reached $6.1 billion across 137 deals, the highest annual amount raised since 2021, with activity underpinned and led by PsiQuantum, Groq, and Cerebras Systems. Additionally, we saw several public-private partnerships aimed at accelerated AI-focused data center development announced across the globe, headlined by the $500 billion Stargate initiative led by a consortium of industry giants, including OpenAI, SoftBank, and Oracle. Reinforcing the rush to expand data center capacity, hyperscalers throughout the year continued to make significant investments in infrastructure development. Meta unveiled plans for Hyperion, a new AI data center with an unprecedented 5 GW capacity, designed to power its Superintelligence Lab, with a footprint estimated to span the size of Manhattan. According to public filings and financing news, the company has arranged a $27 billion financing to underwrite the Louisiana-based data-center campus, making it one of the largest single private-sector infrastructure investments in tech history. Meanwhile, xAI accelerated deployment of its own facility, Colossus 2, converting a decommissioned industrial site into what is now the fastest-growing gigawatt-class AI training campus in the world, achieving record-breaking capacity milestones through a vertically integrated infrastructure approach.

Catalyzed Energy Innovation

Score: 3

Massive funding rounds, hyperscaler energy procurement, and public-private investment momentum propelled nuclear, geothermal, and next-gen energy systems into a new phase of accelerated commercialization.

Several sizeable and high-profile energy innovation funding rounds took place throughout the year, including Commonwealth Fusion System’s $863 million Series B and Helion’s $425 million Series F funding rounds, the former of which secured more than $1 billion in future energy sales for its first ARC reaction. Additionally, the Pennsylvania Energy & Innovation Summit showcased more than $90 billion in planned nuclear, geothermal, and AI-driven infrastructure investment, signaling a decisive public-private pivot at the global level with Google’s landmark geothermal PPA in Taiwan and France dedicating one gigawatt of nuclear capacity for national AI compute. More broadly, hyperscalers are now directly reshaping the energy landscape, with AWS purchasing 1.92 GW of nuclear capacity, Google advancing next-gen reactor collaboration with Westinghouse, and the U.S. Department of Energy recently providing Constellation Energy with a $1 billion loan to finance the restart of Three Mile Island nuclear reactors for Microsoft.

Accelerating Identity & OT Security Threats

Score: 3

Collectively, evolving enterprise risk surface dynamics have yielded a threat environment in which identity attacks, infrastructure-level exploitation, and OT-surface expansion are converging more rapidly than enterprises can adapt.

2025 marked one of the most disruptive years on record for identity- and OT-centric cyber incidents, with cascading outages and breaches triggered by identity compromise, system misconfiguration, and failures in embedded asset and software supply chains. Identity-driven breaches continued to dominate the threat landscape, with phishing-based attacks overtaking compromised credentials as the leading initial attack vector, accounting for 16% of breaches and costing organizations an average of $4.8 million per incident. At the same time, attackers increasingly exploited the widening seams created by IT-OT convergence. As highlighted in our Escalating Threats: The Surge in Enterprise Vulnerability Exploitation research article, vulnerability exploitation is exhibiting a marked shift in zero-day activity toward security appliances, VPNs, and core network infrastructure, enabling deeper and more persistent operational access. These vulnerabilities compounded a rapidly expanding exposure surface, with more than 43,500 newly reported CVEs in 2025, representing 16% year-over-year growth and overwhelming organizational patching capacity. OT defenders reported parallel pressure, with 64% citing increased ransomware targeting, 57% observing heightened nation-state activity, and 52% experiencing rising supply-chain compromises, underscoring that adversaries are scaling faster than OT controls and workforce capabilities can mature.

Identity-centric threats are expected to intensify as enterprises begin grappling with a new and largely ungoverned risk layer: non-human, agentic AI identities. As autonomous systems gain the ability to initiate actions, make decisions, and interact with infrastructure at machine speed, enterprises will face an unprecedented expansion of high-privilege, difficult-to-monitor identities that adversaries can exploit at scale.

.png)

Defense, Telecom, and Space Boom

Score: 2

Reflecting a more tempered partial boom, defense and space segments experienced relatively strong, albeit concentrated, capital inflows and innovation tailwinds, offset by muted telecom activity.

Driven by secular tailwinds, geopolitical dynamics, and technological advances, 2025 was one of the strongest years in recent history for defense and aerospace, albeit less so across telecommunications. According to Pitchbook, as of 3Q25, there has been nearly $40 billion in global VC funding across defense technologies, already a 7% increase of 2024’s annual total and the second-highest aggregate annual amount on record, behind the $51.2 billion raised in 2021. Global VC exit activity has similarly exhibited relative strength, reaching $22.6 billion, the third-highest amount on record. Alongside heightened defense spending and government initiatives, space and aerospace-specific technologies also experienced a notable surge, with global VC activity reaching $12.6 billion this year and marking a 60% annual increase, according to data from Crunchbase. Additionally, during the first three quarters of 2025, defense startups were allocated 1.3% of Pentagon contracts, more than double the 0.6% proportion from the prior year. However, offsetting full realization, PE and M&A activity have been more mixed and subdued, with the former falling below pre-pandemic annual averages and the latter only marginally higher than 2024. Furthermore, the telecommunications industry failed to exhibit the same enthusiasm and accelerating momentum as the defense and aerospace industries, both of which exhibited a relative degree of concentrated activity and traction.

Multimodal AI & Computer Vision Advancement

Score: 3

Breakthroughs in multimodal benchmarks, video understanding, inference efficiency, and enterprise adoption confirmed that computer vision and multimodal AI were among the fastest-advancing technologies of 2025.

As expected, building on a momentous 2024, AI’s pace of innovation and advancement continued to accelerate, with particular momentum behind multimodal model sophistication, capability, and application. Beyond continued enterprise adoption, with notable computer vision applications in the aforementioned aerospace and defense industries, there were significant strides in multimodal performance. In evaluating the comparative performance of select leading models across multimodal performance benchmarks, including Video-MME, MMMU, MMMU-Pro, DocVQA, ChartQA, and TestVQA, 2025 models exhibited an average performance increase over leading 2024 models of 5%, with only the latter two benchmarks exhibiting a degradation in annual performance. Additionally, Stanford’s 2025 AI Index Report found that vision‑language systems now match or exceed human performance on key benchmarks, exhibited by Visual Commonsense Reasoning (VCR) scores that climbed to 85.0 and video‑understanding models achieving 67%+ accuracy on the MVBench benchmark, marking a nearly 15% increase since 2023. Reinforcing the accelerating pace of advancement and improvement, the scores of leading models have more than doubled in their Artificial Analysis Intelligence Index score, a notable ramp up from the improvement rate exhibited. With this, leading foundation vision-language models improved inference efficiency by nearly 30%, materially lowering technical, resourcing, and time barriers for real-time multimodal applications.

Marginal Quantum Progression

Score: 3

Headline breakthroughs in qubit stability, quantum advantage, hybrid-system collaboration, and investment momentum marked 2025 as a pivotal year of measurable but still early-stage quantum advancement.

Although still years away from commercial viability, several breakthroughs and developments collectively drove marginal incremental progress toward tangible applicability. During the first nine months of 2025, a reported $3.8 billion in equity investment across quantum computing companies, nearly triple the entire amount of 2024 and anchored by several headline investments, including PsiQuantum’s $1 billion Series E, Quantinuum’s $600 million investment, and SandboxAQ’s $450 million Series E. Developmentally, Caltech’s neutral-atom team unveiled a 6,100-qubit array capable of maintaining 13-second superposition coherence, marking a ten-times improvement over prior systems, and a foundational step toward scalable, fault-tolerant error correction, while Microsoft, Amazon and Google, which demonstrated the first independently verifiable quantum advantage, all announced quantum infrastructure and architecture initiative progression.

Conclusion

2025 ultimately proved to be a transformative year in which the accelerating forces of AI, energy innovation, and escalating cyber risk converged to reshape the global technology and investment landscape in profound and lasting ways. The Vation Ventures R&I team’s prediction evaluation highlights how strongly these currents reinforced one another: the rapid expansion of hyperscaler data center footprints intensified demand for next-generation energy systems; the widening enterprise attack surface elevated cybersecurity from a defensive priority to a market accelerant; and breakthroughs in multimodal AI and quantum computing pushed the technological frontier further into realms once considered distant.

As we look ahead, the interplay among these domains is poised to grow only more complex and more consequential, reinforcing the need for foresight, adaptability, and a holistic understanding of the technological forces now reshaping global markets. Get in touch today to learn more about how our team can help you navigate the coming year with actionable research and insights.